Lurking in the dark... store

Kirana-tech is in fashion, and something ominously called dark stores is gaining popularity. Is this the Uber moment for grocery retail in India?

Thirteen years ago (2007), I wrote a paper on why kirana stores should collaborate (with each) to set up a marketplace and provide doorstep delivery (the hyperlocal was not a term in those days). I argued that collaboration would make sourcing cheaper and offset the cost of doorstep delivery, simple logic. The marketplace would be structured as a cooperative. Naive and impractical, I agree, but it exciting to talk about such models. Cooperative is a good legal structure, but not everyone can build Amul.

The kirana stores felt was ignored all through the modern-trade boom, e-commerce boom and hyperlocal food delivery boom in the last decade. There were tones of articles highlighting the gradual decline of friendly neighbourhood stores. Of course, many trade associations seeking protection - multi-brand retail was blocked.

Cut to 2020, and the kirana stores is a hot topic. Not because of COVID19, but because of Jio Mart (Jio Platforms). Reliance Industries, through their venture Jio Platforms has launched a grocery retail business by collaborating with Kirana stores and using WhatsApp as a discovery channel.

Why is this new? And why has Jio Platforms captured everyone’s imagination? For starters, the insane spree of fundraising, but more critical is Jio’s execution muscle. Jio went from zero to 307 million subscribers in four years flat; this led to the demise of small operators and consolidation among big players. This execution track record creates excitement around Jio Platform’s Kirana play. Moreover for India (1,2, N) internet is WhatsApp.

But Jio is not the first one to look at kirana network. Many have tried in the past, but no one could make a real dent. Retail is brutal, low margin business. Jio’s money coupled with a well-oiled retail supply chain (Reliance Retail is one of the biggest retailers from grocery to gold), technology focus and WhatsApp as frontend makes it a very potent player.

What is all this got to do with dark stores? Oh, what is a dark store? Sajith Pai, a long-time media executive, turned VC in his early notes on the Jio-Facebook deal: implications and second-order effects wrote about dark stores as one of the new ideas to emerge from the possible success of Jio Mart. He writes, …what cloud kitchens are to Swiggy, dark stores are to Jio Mart. To put it simple words, a dark store is a grocery store with no walk-in customer, it leverages data to make sure the right inventory is on hand. Consumers who order ahead get the items delivered at the doorstep or available to kerb-side pickup.

It’s an intriguing concept, but here are some follow-on questions - is this a new concept? Where do Kirana stores fit in? Is there a play for new startups?

More on dark stores

Is dark stores a new concept? Short answer, no.

Dark stores are micro-fulfilment centres (small warehouses) used for storage and last-mile delivery of merchandise. Such fulfilment centres have been around for quite some time. Sainsbury in the UK introduced them in the early 2000s, again in 2012. Closer home Dmart (click-and-collect model under Dmart Ready available in few cities), Bigbasket(home delivery in all cities), Amazon have network smaller warehouses spread across a city.

Possible benefits of micro-fulfilment: for consumers, faster delivery (on-demand, 2-hour hyperlocal window), better experience; for brands or marketplaces, reduced cost of operations, access to consumer-level data, access to sub-Pincode level inventory projections, and storage to support greater product availability.

Owned-and-operated micro-fulfilment centres are not new. What’s new is the possibility of dark-stores-as-a-service or micro-fulfilment-as-a-service business.

Where does the kirana store fit-in?

India has roughly 6.65 million such stores, given our population that translates to 1 store for every 48-50 households. Each store has approximately 500-700 SKUs, sometimes even more. Kirana stores usually carry 20-22 days worth of inventory. Converting even a part of this network into a tech-enabled fulfilment centre can unlock tremendous value and customer loyalty. But it is hard to crack this network - requires significant capital, technology and persuasion to create buy-in - Jio is familiar with this playbook. Jio Mart has onboarded 6000 stores in Thane as trial and already working fine-tuning its model.

Jio Mart is not the first entrant in this model that title goes to Grofers (B2B space was led by Metro Cash and Carry). Through 2019, Grofers built a network of 700 branded Kirana stores and planned to grow the number to 1000. With COVID-19, not sure where the plans stand. We also Flipkart with a similar kirana engagement initiative.

How does the kirana-as-fulfilment model work? Platforms (such as Jio Mart, Grofers) provide full-stack support to the kirana store, take over the operations more or less. The support includes point-of-sale (POS) machine, inventory tracking, replenishment based on predictions, last-mile delivery (not clear how Jio Mart will do this, for now, it seems like a kerb-side pickup) and customer access (discovery via own app, WhatsApp for Jio Mart). Early attempts failed to make an impact because they never had information on inventory on hand - the focus was on POS and discovery. Swiggy and Zomato offer discovery and delivery, not sure how they will make any money on such operations.

There are some advantages of Jio Mart model - Jio Mart can negotiate better terms with FMCG brands, use granular data to up the private-label game, influence customer behaviour to improve the margins, improve the ROI for the stores in the network.

One unknown at this point is how Jio Mart will enable discovery. The Swiggy/Zomato approach of listing stores may not work - stores will have to pay for the listing, improve search rank etc. Treating stores just as fulfilment points may work better - allow pooling of items from multiple centres if required.

What does the store owner bring to the table? Real estate, capital for inventory or bears the risk for any loan arranged by the platforms. For Jio, zero/minimal fixed costs, limited capital risk makes the entire operation asset-lite yet extremely data-rich. That’s the game!

The new breed of dark-store startups

Yes, we will see exciting models emerge, from simple ones to tech-driven. To better understand the models, it will be good to know the key drivers of the retail operations. A highly simplified list, but it will give you the gist.

Inventory - faster the circulation of stock the better - it’s ideal if all the stock sells-out in the expected time. Also, it is crucial to carry a broader range of SKUs to cover most customer use-cases.

Real Estate and Human Resource - this is a high fixed cost in retail - prime locations cost more but provide better access to customers. People run the supply chain (autonomous delivery is a few years away); the current pandemic is a fantastic example. If you are struggling to find a delivery slot on Bigbasket, that’s because they have very few delivery folks or warehouse operators.

Margins - a typical kirana store might make 10-12% margin and distributor around 2-3%. With such thin margins, cash flow is critical for business, faster the better, tied with Point 1.

Technology - linked to Point 1 and 3, the aim is to use technology to streamline operations, increase margin. More efficiency means more margin.

Capital - access to capital will define the scale of operations.

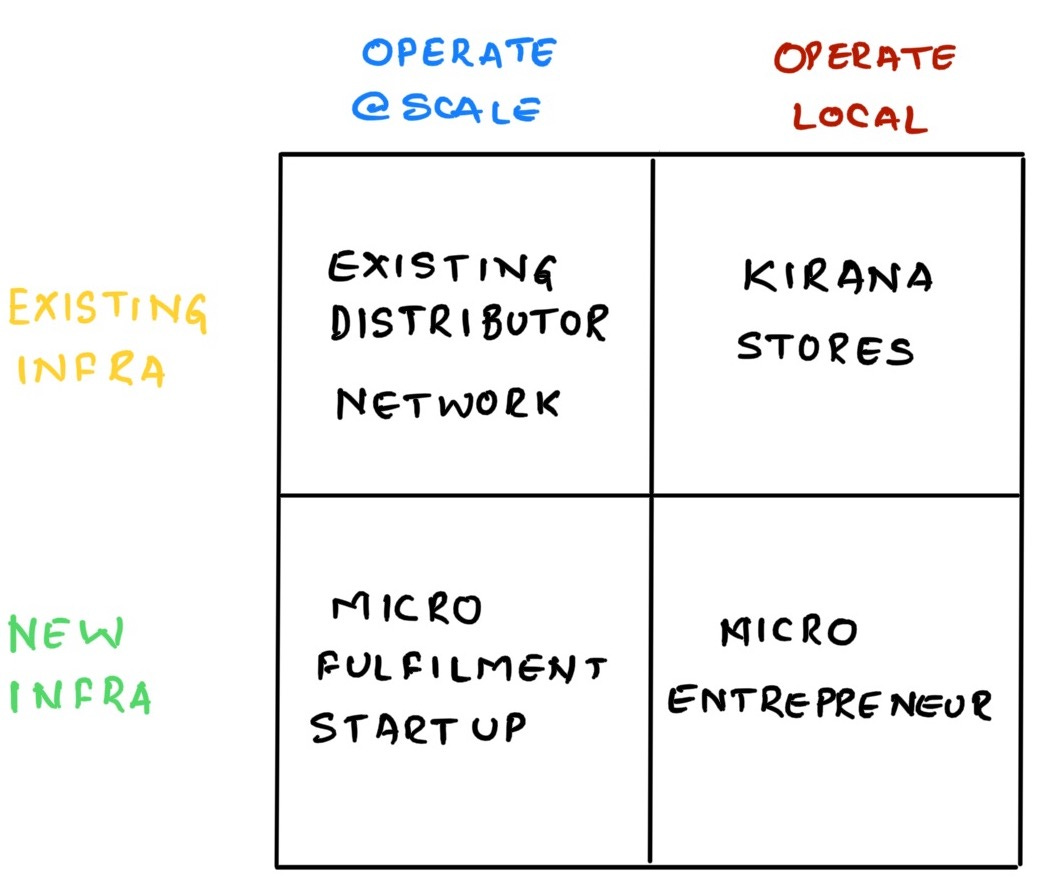

Obviously, there are more factors, but these are the key ones we will use in the assessment. With these factors in mind, let’s look at the potential participants in

Existing Infrastructure - entities with existing warehouse network, retail footprint

New Infrastructure - greenfield setup with a completely new network of warehouses

Operate at Scale - large enough operations to serve multiple locations in a city

Operate local - service area is limited to 2-3 kilometres

The entities best placed today are the ones with existing infrastructure - the CPG distributors, and Kirana stores.

CPG distributors already have a warehouse and have the capital to expand their warehouse footprint. Distributors are aware that cash flow is key to sustainable operations and hence better partners. But distributors fall short in technology adoption, decisions are based on experience and not data.

A kirana store can service a smaller area, fixed cost, capital and margins are already set. The walk-in business will subsidise the fixed costs of fulfilment operations. Jio Mart and Grofers will provide technology to automate inventory management. Seems like win-win for both Kirana owners and platforms, but with data platforms may grow more robust.

Micro-entrepreneurs are individuals who set up 1-2 dark stores and list on platforms such as Jio Mart. Traditionally, Reliance has encouraged such endeavours with a promise of decent ROI. Similar to driver-owned cabs enlisted on Uber/Ola - we all know how ROI declines over the years. Micro-entrepreneurship will not work, but there will be takers.

Lastly, the most interesting one is micro-fulfilment startups or dark store startups. Dark store space may not be a complete greenfield space. Existing logistics players such as Delhivery, LoadShare etc. are already talking to brands on how they can help, will it be a fulfilment play? We will have to wait. Logistics startups do seem to have a headstart for now. Positives of fulfilment startups (a) better consumer experience, shorter delivery times (b) control over consumer experience for the brands.

We will also see newer fulfilment startups emerge with technology-led operations. Check this video to visualise what a micro-fulfilment centre might look like ideally; you can also look up some of the startups in the West. An important distinction to note is that unlike a kirana store or a CPG distributor, a dark store company provides just fulfilment-as-a-service, might not make investments in inventory. As consumers loyalties get tied to delivery speed, micro-fulfilment sites will rise to meet such expectations.

Note: A micro-fulfilment making inventory investment will be very interesting but the model would be riskier.

What will make a dark store or fulfilment-as-a-service startup work?

Fixed Cost and Capex

Firstly, manage real estate costs. High real estate costs render many a business uneconomical, look at the restaurant sector. Innovative approaches such as renting part of an existing warehouse, working with apartment complex etc. may be necessary to manage fixed costs. Secondly, right-sized capex is important, availability of space will constrain it anyway.

Automated, Data-driven Operations

Operations have to entirely automated, data-driven - visibility of inventory across the network, granular predictions are SKU-Store (each fulfilment centre is a store) daily to sense demand and relay the information back to brand/marketplace/platform. Predictive alerts that inform brands about possible out-of-stock or wastage. Startups have to build these capabilities in-house or work with other technology startups in the domain. The ecosystem has startups such as Algoshelf (disclaimer: the author is part of the team), who provide AI-enabled inventory management solutions out-of-box; robotics startups such as GreyOrange which offers fulfilment operating system to manage a warehouse; logistics planning and automation solutions from locush. Dunzo and Bounce for last-mile possibly.

Technology and Digitisation

API-first technology stack, inventory, stock transfer, product recall, return everything should be an API - look at Shopify fulfilment API for more details. Easy software integration will make it easy for brands and platforms to integrate. Corollary to API requirement is the digitisation of processes in the brand’s supply chain. The API-first approach will enable the exchange of granular data between brands and dark store network - traditionally, brands never get granular data, customer data from the retail channel.

Pricing

Transparent and straightforward pricing will be good. A percentage of merchandise delivered with agreed service levels seems like a good strategy or a mix of storage, technology and delivery based fees might work as well.

The goal of a fulfilment-as-a-service platform should be to use technology to improve efficiencies, lower the cost of operations.

Will platforms such as Jio Mart, Grofers collaborate with dark store startups? Only time will tell us, right now, their focus is on kirana stores. But CPG brands that went DTC during the pandemic, experimenting with stores on Swiggy and Zomato might consider partnering with dark store startups. The temptation to own the customer relationship will rise over time and brands cannot afford to ignore DTC anymore - some have learnt this the hard way in the last couple of months.

Consumer behaviour is changing, at least in urban India, and brands need to master the changing dynamic fast.

Closing

Platforms such as Jio Mart are great for consumers but not so great for brands. If platforms can balance private label play and share data with brands, there may be a win-win, but that’s hard. Look at the restaurants vs food delivery platforms dynamic; restaurants are planning to collaborate and start a delivery infrastructure of their own. We have to wait and watch.

Some day, brands have to set up a direct channel with consumers and fulfilment-as-a-service is one such channel.

For now, it seems like Jio Mart is kirana store’s Uber moment. I’m sure, there will an Ola moment as well :)

This is a brilliant deep-dive—especially the historical perspective on kirana networks and how the evolution of fulfillment models has created new leverage points. What stands out is how Jio Mart’s entry isn't just about tech or capital but about understanding and integrating existing infrastructure intelligently (kirana + WhatsApp + last-mile).

Your analogy of kirana stores as “micro-fulfillment nodes” is spot on. The challenge, as you rightly noted, lies in incentivizing tech adoption at scale—especially in a network that has traditionally resisted change due to low margins and informal operations. It will be interesting to see if Jio’s cooperative-style playbook can unlock true shared value or if it gradually shifts to a data-dominant platform model where the balance of power tips again.

Also, loved the mention of “dark-stores-as-a-service” as a potentially investible space. Curious to see whether logistics-first players or tech-first startups will win here—or whether hybrid models like Delhivery meet Shopify is the way forward.