Brands setting up DTC in a jiffy, will it stick?

Incumbents are executing fast, willing to collaborate with everyone - behaving more startup-like. The insurgent brands are playing catch-up!

Last month, Pepsi (US) launched two direct-to-consumer portals PantryShop.com and Snacks.com. The team at Pepsi went from concept to public launch in 30 days flat. The offerings on both portals appear to be rooted in good consumer insights and current market condition. Unlike conventional e-commerce, Pepsi offers product bundles. Each bundle is designed around a specific consumer need or use-case. This is interesting because product bundling plays into changing purchase behaviour (stock the pantry, make at home) and also works well for unit economics (The average cost to deliver a single bag of Doritos is the same as a $20 snack box, so it is better to sell as a bundle).

Pepsi has an extensive product portfolio, and bundling multiple brands offers customers a new value proposition. The “Rise & Shine” bundle for breakfast, the “Workout & Recovery“ bundle for fitness, are great examples. Consumers are looking to reduce grocery trips or contact with delivery personnel, so bundle work well. Bundling allows Pepsi to make offerings distinct from retail shelves, avoiding any channel conflict.

Side Note 1:

With limited data on cost-to-serve it hard to make a concrete assessment of unit economics. Brands are willing to absorb the cost for now to increase availability and access.

We can see a similar trend among FMCG brands in India. There is a transition from setting up shops on delivery apps to setting their own webshops - likes of Marico, and ITC has setup webshops. Setting aside the old ways of taking things slow, both DTC portals were set up in less than 45 days. Not to be left behind the insurgent brands too launched their web stores, some examples Epigamia, Raw Pressery.

Here are some observations on the early DTC moves for both legacy and insurgent brands in India:

Not much innovation in product offerings (compared to Pepsi above). Both Marico and ITC can easily create need-based bundles, instead, they chose to set up regular e-commerce. Subscriptions on ITC is more a re-order workflow reversed. Bundles are an opportunity to create a different value proposition.

Brands are happy to push bigger pack sizes or value-packs to increase order value. Multipacks/value packs/special packs are used to avoid channel conflict. Luckily plays well with current consumer sentiment of stock-up.

Single category brands (most insurgents) will need to innovate on the value proposition, work on cross-brand (external) collaboration to increase order value. Raw Pressery’s subscription offer is interesting.

Insurgent brands with better distribution or those that fell under essential category have not made any visible DTC moves yet e.g. iD Foods, Veeba Foods. Essential brands proliferated in the last couples of months, iD Foods’ sales grew by 25% in March 2020.

Brands seem to be optimising for availability, for now, so higher cost-to-serve is fine.

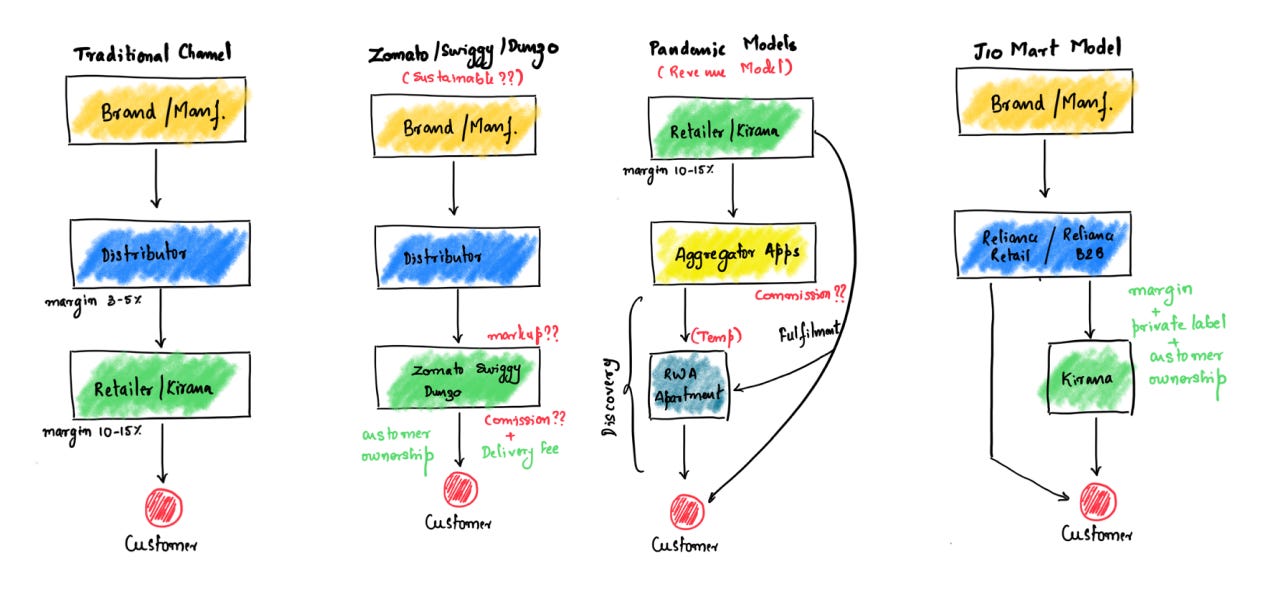

From the above points, it is clear that no one has a playbook, at best it is work-in-progress. Everyone says DTC is here to stay, but there is no visible long-term strategy. The model of a distributor as fulfilment and Dunzo/Zomato/Swiggy as last-mile is at best a proof-of-concept.

Side Note 2: Second-order effects of FMCG brands going DTC

DTC might become a new R&D channel for brands to experiments new products, packaging, product bundles and offers. Some of the online learning may make its way into physical retail. Bundles might also influence product placement, e,.g. Oats and almond milk are next to each other on the shelf and promotions

Legacy brands will increase digital spend to drive customers to their web properties; this will increase the CACs and CPMs. Insurgent brands will have to get innovative to reduce CAC on digital channels. Ad rates have plummeted significantly over the last two months

Using data to craft marketing will take centre stage as brands will strive to balance business objectives and CAC

Will DTC stick as a channel?

Has the pandemic changed consumer behaviour permanently in favour of DTC (online in general)? It is too early to call; we have not seen any decades happen in weeks kind of data in India yet. Consumers have moved to kirana stores more than online. Due to a shortage of warehouse workers and delivery professional, online was hit-and-miss.

DTC is a new channel in India - very few insurgent FMCG brands are digital-first. The only exception in the food space is packaged meat providers such as Licious, FreshToHome and Fipola. Insurgent brands have focused on traditional retail distribution and e-commerce. The current pandemic has forced the insurgents to explore DTC. Without a proper playbook to work with, the consumer experience with DTC will remain inconsistent for some time.

It is going to take time for brands to build a proper DTC offering and here is why.

Changing consumer behaviour is hard

It has been thirteen years since the founding of Flipkart (nine years for Big Basket) and many more players entered after that - the share of e-commerce is 2-3% of the FMCG market. Modern Trade (Big Bazaar, D-Mart, etc.) even after two decades of existence accounts for 11-13% of the FMCG market. Of course, these numbers will possibly double for Tier I cities. But the bulk of the market continues to be traditional retail, and although this segment is declining it remains resilient - overall, it may decrease to 80% from 85%. So, channel switching happens over an extended period - yes, the pandemic has accelerated some behaviour changes, but there is no clear evidence of a permanent switch.

Demonetization is another case-study on consumer behaviour. Consumers moved from cash-to-card-to-app in a matter of days. Everyone from kirana stores to street vendors had a QR-code to accept payments. But as the cash circulation improved transactions returned to cash (the QR-code stickers are now a relic from 2016). The effect of demonetisation lasted for 50-60 days, enough to influence behaviour change, but that did not happen. UPI payments are growing, it took three years to achieve exponential growth.

Going by past behaviour, DTC and online grocery will not see sustained adoption over medium-term. Also, consumers have rediscovered their love for kirana stores, and a sizeable market may stay there for a while.

That said, there are good indicators (Jio Mart with kirana partnerships for example) that e-commerce and online grocery might gradually replace a sizeable share of the modern trade market in Tier I-II cities (medium-term).

Brands have to decide whether DTC is a band-aid or a future channel

Legacy brands stole a march on insurgent brands during the lockdown on the back of a good distribution network and a strong balance sheet. Out of sight, out of mind was a real threat for insurgent brands, and hence DTC operations were set up in a jiffy. All good and exciting, but it is not clear whether DTC is a band-aid or brands are serious about building a new channel.

Side Note 3: Unlike their peers in the high-value DTC categories such as a mattress, commodity FMCG brands will find it hard to build a scalable, sustainable DTC business. Limited portfolio means lower product bundling options, higher cost-to-serve and higher CAC.

No brand wants to disturb traditional retail channels. So, it is essential to understand a brand’s expectations from DTC. What are the objectives for a direct channel:

R&D for new products, package, bundles offers and trials

Control the brand experience and build a relationship with the customer

Build omnichannel marketing and sales engine

Legacy brands have been experimenting with (1) through contests etc. but in future, it might be (2) and (3) - see Pepsi above. If brands are serious about DTC then they have to invest in understanding unit economics, product development (cannot compete with existing products), customer acquisition (a hook) and fulfilment infrastructure. Just setting up a webshop using Shopify and trying online will not cut it.

Both insurgents and legacy brands have limited, or no DTC experience - right now both work in wholesale. In the absence of a playbook, both insurgent and legacy brands will be experimenting a lot in the coming months. Continuous tinkering means inconsistent customer experience - consumers may switch back to existing channels.

Whether DTC will stick? Considering the two factors above, over medium-term, it will have limited uptake, customer experience will not be great. Over time as the brands figure customer acquisition and fulfilment with a manageable cost-to-serve, DTC will be a sizeable channel.

Making DTC happen

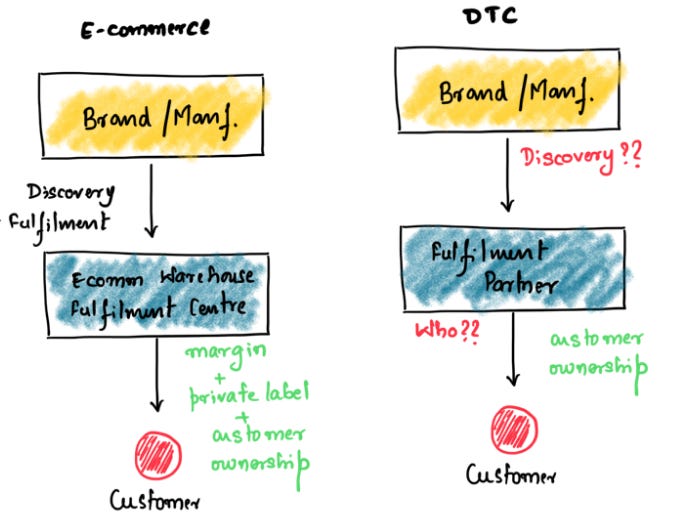

Setting up a webshop is the easiest part, the two most important aspects to get right are customer acquisition and fulfilment. Yes, brands have to get these right every day to grow and retain the customer base.

Customer Acquisition

Customer acquisition is very expensive - billions of venture capital dollars have been (continue to be so) spent on customer acquisition. The key questions brand must pose themselves - why should a consumer visit our portal? If they do visit, make a transaction, will they come back? What will make them come back? There are no easy answers.

It starts with the product itself, followed by a killer value proposition for direct engagement. Brands have to develop a strategy for bottom-up customer engagement, community building and engagement - these are time taking endeavours but may turn out to be far more cost-effective than spending millions on just digital ads alone.

We have some bright spots in the current insurgent landscape - Raw Pressery has done some interesting things with its DTC shop. Raw Pressery offers such customers pre-paid subscriptions, and customized multi-packs, this works well for its health-conscious customer base that consumes juice as part of nutrition every day. Moreover, subscriptions mean upfront cash for the company. Coupled with good fulfilment experience, Raw Pressery will retain its customers, may add more and also avoid channel conflict.

Isn’t it easy to acquire customers through Facebook? No, Facebook, Google ads are a suboptimal acquisition channel, a brand might see some sales but no meaningful customer engagement or insight. On Facebook and Google, the customer relationship is owned by the platform and the brand. It might be wise to build a customer-centric engagement strategy, Facebook/Instagram can be leveraged but no point outsourcing acquisition to these platforms completely.

Customer acquisition is a critical aspect of DTC and deserves more in-depth treatment, more in future articles.

Side Note 4: The likes of Amazon, Flipkart, Zomato and Swiggy should be treated as another discovery channel (retail channel) and not DTC facilitator.

Fulfilment

“Partners“ was the buzzword in all FMCG sales calls over the last eight weeks. Brands were (I believe they still are) willing to partner with anyone with a reliable delivery fleet, and a discovery channel was a bonus. We can see brand stores on Zomato, Swiggy, Dunzo. Even many non-food/non-logistics companies joined the last-mile fulfilment business - MakeMyTrip, NoBroker, StoreSe, BharatPe etc.

Side Note 5: one of the most exciting examples of collaboration was the tie-up between ITC and Dominos (Jubilant Foodworks). Dominos in India has around 1,325 stores across 282 cities, even if a few hundred stores were operational that is tremendous last-mile outreach for someone like ITC.

Why so much focus on fulfilment? Once the product succeeds, and customers are acquired, what enables a brand to retain a customer is the availability and on-time delivery of the products i.e. fulfilment.

Serious DTC aspirants have to assess data from existing partnerships and figure a structure that might work and align with business objectives. The fulfilment infrastructure has too many possible players right now; brands should ask how many of these will last to see 2021? Look at the landscape in the graphic below

Operators with a strong balance sheet and inventory-centric model will survive. Others (Pandemic Models in the above graphic) will wither away (no sustainable revenue model, just discovery is not enough). Why? Because (1) It is hard to control customer experience without inventory visibility (2) There is no money in standalone customer discovery - no kirana store will pay a commission in the long run and customer will hunt for a delivery deal.

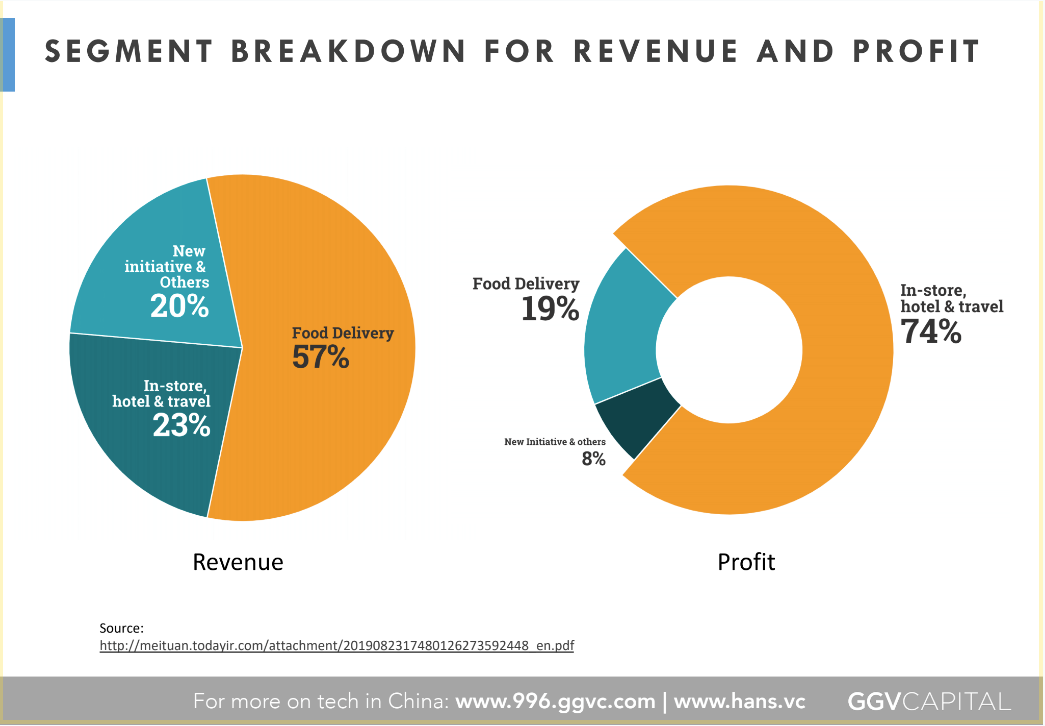

The most likely DTC fulfilment partner for brands in the future might be Zomato, Swiggy (both need a new fulfilment business model) or a new player(s) with a darkstore network. Zomato has some experience because of Hyperpure, but Swiggy, Dunzo have no such advantage. There is no playbook for grocery fulfilment - the closest comparable is Meituan-Dianping (investor in Swiggy) in China. Even Meituan is struggling to make profits from the delivery business, a good share of profits can be attributed to advertisements and travel-centric bookings, see graphic below. So, India will need a new fulfilment playbook to support the DTC channel - one example is the Jio Mart, WhatsApp and kirana partnership.

Brands will need a strong fulfilment partner who can execute the last-mile with efficiency. Such infrastructure players are more critical for the success of single category DTC brands. The landscape will continue to evolve over the next few months, and we will see more player emerge, till then, DTC will move in the slow lane.

Side Note 6: Amazon is a strong contender as a fulfilment provider, but their focus on being a discovery channel, private-label makes them a less preferred option. Brands will continue to sell on Amazon but may not partner for hyperlocal fulfilment.

Side Note 7: One option to set up DTC operation is to acquire an existing DTC brand. Might work in the west but there are no such targets in FMCG space - at least I have not come across any yet.

Closing

So who will win? Incumbents have a jumpstart, but insurgent brands will be back in a few weeks. So it may not be prudent to write-off insurgent brands. DTC is here to stay, it will catch on over the next few years, but it might be completely different from what we’re witnessing right now.

As for the single category FMCG insurgents: until a reasonable playbook emerges (India needs its own playbook, lift-and-shift does not work), they will focus on fixing supply chain issues, improving availability in existing channels and engage with the consumer on digital channels.

In the west, FMCG insurgents start as digital-only brands and transition to physical retail - we have seen this trend across furniture, apparel categories but not FMCG. But in Indian FMCG, the insurgents target the physical retail more (97% of the market), online or digital (Amazon) is used for validation. So, DTC is a new game for both insurgents and incumbents.

As the fulfilment infrastructure and last-mile evolve, there will be more action on customer acquisition, at least from brands seriously interested in the DTC play.

Caught My Eye

In retail, private label is where the profits lie - below are examples of private labels from Reliance on Jio Mart, sold at a price 40-50% lower than branded peers.

PS: I was surprised to see private label toothpaste from Reliance